To cap off our series on fixed income in a low interest rate environment, Portfolio Manager James Arnold evaluates the likelihood of runaway inflation and explores the case for continued low inflation, or potentially even deflation. Weighing the possibilities, James looks at factors such as changing demographics, technological advances, failures of monetary and fiscal authorities, and existing debt levels.

Earlier in this series on fixed income in a low interest rate environment, we explored the merits of owning bonds by reviewing the steady income and incremental returns they provide, their tendency to be negatively correlated with equities, and their inherent hedge against deflation. With this context in mind, we can set our sights on the area we believe is the root cause of investor uncertainty when it comes to bonds: inflation and the potential for ensuing higher interest rates. Despite low current yields, we believe these concerns are what really have clients questioning holding bonds in their portfolio.

As previously highlighted, we believe that the primary reasons investors hold bonds have not actually changed. Furthermore, we believe the case for continued low inflation, or potentially even deflation, has as much merit or more than the case for runaway inflation. This is due to factors such as changing demographics, technological advances, persistent failures of monetary and fiscal authorities to generate inflation, and existing debt levels.

IS A WAVE OF INFLATION COMING?

In the event of a resurgence of inflation, the income stream provided by bonds would likely fall significantly short of that inflation. A sharp increase in interest rates, a likely outcome following higher inflation readings, would cause a sudden contraction in bond prices due to prices and yields moving in opposite directions. We believe that the fear over a sudden spike in inflation combined with the already low yields on bonds today, not just the current low yields bonds provide, is what concerns investors most about investing in fixed income.

At Burgundy, we believe that the notion of a coming inflationary crisis is up for debate. Demographics and technological advancements are strong deflationary forces, and monetary policy has already failed to generate significant inflation since the Global Financial Crisis. The link between fiscal spending and inflation may also not be as strong as we have been taught. Finally, increasing debt loads on consumer, corporate and sub-sovereign balance sheets are likely to act as a headwind to future growth and inflation.

Demographics

Demographic trends are decidedly negative in North America as our population continues to age and the baby boomer generation continues to exit the work force. The birth rate in developed economies has been steadily falling for decades, in many cases well below the replacement rate of 2.1 children per couple. Older people spend less money, often downsize their homes and, without growing children at home, spend less on consumables such as clothes, toys, and furniture. While younger people or parents with young children may not see this in their day-to-day purchases, the composition of our population has changed and is continuing to develop in a way that leads to less overall consumption. This is a powerful and long-term deflationary force that will take decades to reverse.

Technological Advancement

Take a company like Amazon: There is little argument that its technological advancements have made it cheaper to get daily essentials delivered to your house. The same goes for a ride sharing app like Uber, which, if you were a frequent user of taxis, has reduced the cost of transportation. These examples only scratch the surface of innovative technological breakthroughs that have the potential to fundamentally reshape the economic environment. Robotic technology, for instance, continues to simplify and reduce costs in the manufacturing process and every year we see newer and faster computer processors and larger televisions available at a lower cost. With its continued advancement, technology will remain a deflationary force.

Monetary Policy

Central banks globally have been attempting to use monetary policy to generate inflation since the Global Finance Crisis to no avail. Economic theory tells us that low administered policy rates should stoke demand for borrowing and therefore spending. So why hasn’t this happened? Put simply, central banks cannot force anyone to borrow and spend money. They have tried to increase the incentives for doing so, but there are typically several factors that go into any decision-making process and the cost of funds is only one of them. If, for example, consumers already have a significant amount of debt on their balance sheet, they may be unwilling – at any level of interest rate – to borrow additional money. Central banks have tried for the past decade to use monetary policy to stimulate growth and generate inflation with limited success. It may just be the case that deflationary forces are too strong for monetary policy alone to overcome or that other factors are currently more important in the decision-making process to borrow money than a low cost of funds.

Fiscal Spending

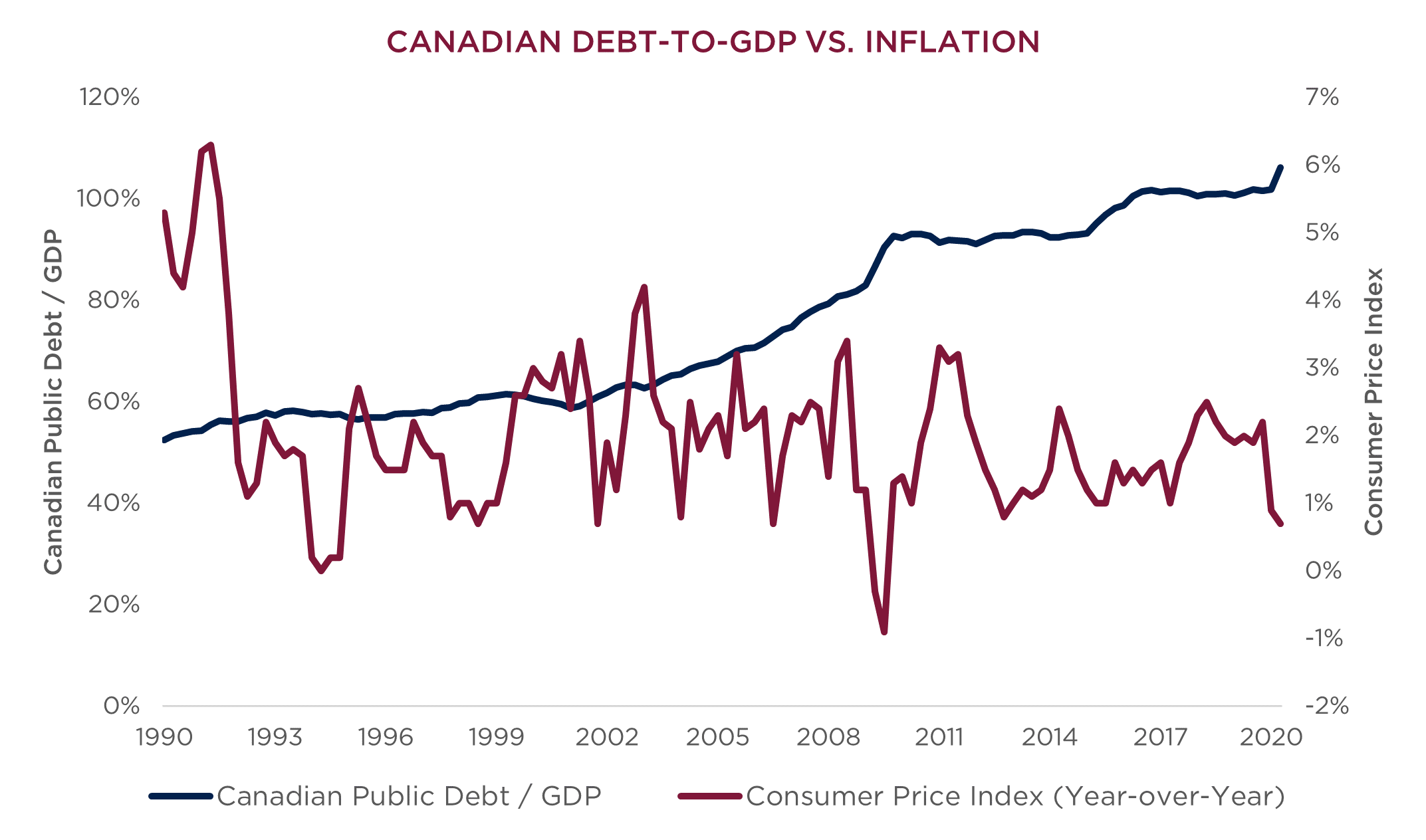

We have long been taught that excessive fiscal spending, especially to the point of large government deficits, will lead to inflation and potentially the crowding out of more efficient private spending. Empirical research shows that the link between deficit spending and short-term inflation is strongest in highly indebted developing economies, compared to almost no correlation in developed economies. Large fiscal deficits, particularly following a large shock to an economy (such as a global pandemic) can replace lost private spending and act as a shock absorber to the broader economy. So, while today’s deficits are the largest we have seen in peace time, they will not necessarily lead to a large bout of inflation as they may be replacing lost spending from the private sector. As we can see in the chart below, increases in debt above and beyond increases in GDP do not necessarily lead to substantial future inflation. While this may seem counterintuitive to some, it highlights that there are many factors that affect the price level of the economy and that singling out one specific input may miss the larger picture.

Source: Quarterly Bloomberg data to June 30, 2020.

Existing Debt

There is no shortage of news highlighting indebtedness in North America today. In Canada, the focus tends to be on stretched consumer balance sheets, while in the U.S. the focal point is on corporate debt. In both countries, there is also significant debt at the sub-sovereign level, which includes state and provincial governments such as Ontario and California. Taking on debt to spend today is the equivalent of borrowing from the future to spend in the present. This dynamic may serve to reduce future spending and therefore limit future inflation. The existing stock of debt, especially on personal balance sheets, is one reason that low rates have not stimulated more spending. Following an economic shock such as the Global Financial Crisis, many consumers were more focused on paying down debt and therefore were unwilling to borrow at any interest rate, even a low one. These trends may well continue, particularly in Canada, as our personal balance sheets remain stretched. Central banks’ ability to increase rates may be limited as this phenomenon may inadvertently put even more pressure on consumers and leave the economy more vulnerable going forward.

THE LANDSCAPE FOR FIXED INCOME INVESTING

Given all the moving parts of a globalized economy, predicting inflation and other economic data is challenging at the best of times. In today’s environment of high fiscal deficits and unprecedented central bank stimulus, the task seems nearly impossible. This is why at Burgundy we focus on investing in companies that can repay their debts regardless of the economic backdrop. We do, however, believe that the current widespread response, which suggests that today’s government intervention will result in significant inflation, requires us to take pause and examine other factors. We do not profess to know how the economy will react to what is happening today, but we do believe that the eventual outcome may not be as simple as previously accepted economic theory suggests.

This post is presented for illustrative and discussion purposes only. It is not intended to provide investment advice and does not consider unique objectives, constraints or financial needs. Under no circumstances does this post suggest that you should time the market in any way or make investment decisions based on the content. Select securities may be used as examples to illustrate Burgundy’s investment philosophy. Burgundy funds or portfolios may or may not hold such securities for the whole demonstrated period. Investors are advised that their investments are not guaranteed, their values change frequently and past performance may not be repeated. This post is not intended as an offer to invest in any investment strategy presented by Burgundy. The information contained in this post is the opinion of Burgundy Asset Management and/or its employees as of the date of the post and is subject to change without notice. Please refer to the Legal section of this website for additional information.