At Burgundy, our legacy of partnering with philanthropic families and managing assets for private family foundations is well established. Recently, a new avenue for charitable giving has gained popularity among our Burgundy families: donor advised funds (DAFs). Join Investment Counsellors Angela Bhutani and Meghan Moore as they delve into how DAFs can enhance your family’s charitable impact and financial planning.

KEY POINTS

-

- Simplify Your Giving: A DAF is a charitable giving account managed by the Burgundy Legacy Foundation. While a DAF has many similarities to a private foundation, it also offers several benefits, such as ease of set-up, no ongoing reporting requirements, and complete privacy.

- Family Philanthropy Made Easy: DAFs can be a valuable tool for involving younger generations in charitable giving and fostering family values in philanthropy.

- Flexibility for Life Changes: DAFs are ideal for time-sensitive situations like business/property sales or life events such as divorce, inheritance, or estate planning. They allow you to make a charitable contribution now and recommend grants to your favourite causes later.

When it comes to charitable giving, you have options. This guide breaks down the two popular family giving options, a private foundation and a donor-advised fund, to help you choose the right fit for your philanthropic goals.

Transcript

What is a DAF?

As Investment Counsellors, we work with many philanthropic families or individuals who are interested in putting in place a longer-term plan for their giving, for themselves, and possibly for their next generation. Donor advised funds deserve attention because of the convenience, the simplicity, and the privacy they afford. We are happy to offer them through the Burgundy Legacy Foundation.

A donor advised fund is a charitable giving account, held within the Burgundy Legacy Foundation. Donors can choose the name of their Fund, oftentimes using their family name, such as the Smith Family Fund. You may hear the short form “DAF” or “giving fund” to describe these structures.

A DAF has many similarities to a private foundation in that it allows families to support charities over many years; however, it’s much simpler to establish, with the application and setup taking only a few days, and much easier to manage as donors don’t have to worry about reporting or governance requirements (these fall under the responsibility of the Burgundy Legacy Foundation). Contributions to a DAF are treated as donations, so families can receive their tax receipt in that calendar year; however, they are then able to take their time with thinking through what charities they’d like to support. And since the DAF assets are invested and allowed to grow and compound tax-free, this helps to increase the amount that can be directed to charities over time.

Ideal donations are securities, like mutual funds, pooled funds, or stocks, that have appreciated in value. Not only do donors receive a tax receipt for the value of the securities donated, but the capital gain on those securities may be exempt from tax when donated in kind.

Donors have the ability to recommend what charities should receive grants from the DAF over time. As a DAF holder, you might want to also think about appointing a successor, someone who might continue providing recommendations once you’re no longer able to. Should you or your family later on decide to set up a private foundation, the assets of the donor advised fund can be granted out to that foundation.

DAFs vs. Private Foundations: What’s the Difference?

DAFs and private foundations can help to achieve the same objective: providing an immediate tax benefit while allowing you to give to your preferred charities over time. But where DAFs really stand out is in their simplicity.

- DAFs are easy to open, similar to setting up an investment account or TFSA, taking only a few business days.

- As a DAF holder, you have no ongoing CRA or administrative responsibilities. This simplicity allows you to focus on what matters the most: selecting your charities or areas of impact and perhaps incorporating family into these important discussions. In contrast, private foundations are costly and time-consuming to start, often taking months, with ongoing legal, accounting, and compliance tasks.

So, a DAF offers similar benefits to a private foundation, but without a lot of the complexity and added costs. This makes DAFs a perfect solution for busy individuals and families who do not have the capacity to take on more administration. And regardless, the low-cost nature of DAFs might mean more of your dollars can go directly to the causes most important to you.

- Another distinct benefit of DAFs is that they offer complete privacy, if desired. Private foundations must publicly disclose their financial information, board members, and grants made. Many donors prefer to give anonymously and may wish to keep details surrounding the size of their charitable assets and grants private.

With a DAF, you determine which information, if any, is shared. You will always have the option to receive recognition for your generosity if you choose, but it is always at your discretion.

A DAF IN ACTION

Here’s an example of how this would all work.

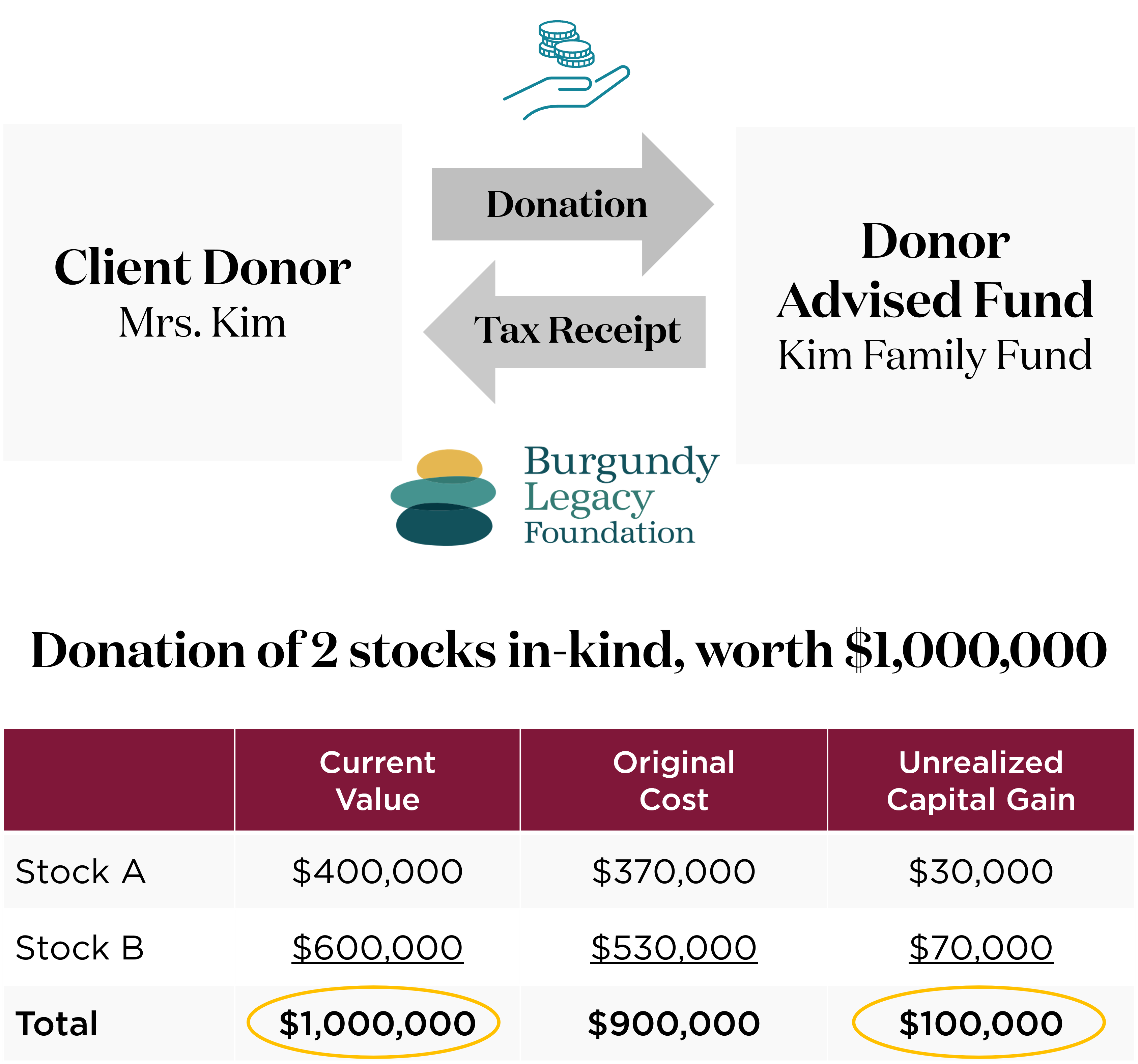

Mrs. Kim has decided to set up a DAF and plans to collaborate with her daughter in supporting women’s healthcare initiatives. The DAF name that they choose is the Kim Family Fund. With the help of the Burgundy Legacy Foundation and her advisor, she puts in place a plan to donate two stocks in kind, with a collective value of $1,000,000, which includes capital gains of $100,000. The stocks will be donated from her personal non-registered account. A signed letter is sent to her broker requesting the transfer in kind.

Once the shares are received a few days later, the Foundation issues a tax receipt for the value of the stocks on the date they arrive. The stocks are then immediately sold and reinvested in a balanced fund in the DAF. In addition to the tax credit on the value of the shares donated, the $100,000 capital gain will also be exempt from tax. Later that year, Mrs. Kim and her daughter meet to review their DAF statement and discuss charities they want to support. They send a request to the Foundation, recommending that 5% of their DAF be granted to a local hospital, for which they would like to be recognized. The charity receives the grant shortly thereafter.

Incorporating DAFs Into Your Planning

Beyond the most common case of using a DAF as part of long-term philanthropic planning, here are some scenarios where DAFs can be useful:

- Engaging Younger Generations: DAFs can be a useful tool for involving younger family members in philanthropy and passing down family values. Given the simplicity and ease of setting up a DAF, there is so much customization that can be done to suit a family’s needs. We see families setting up a dedicated DAF to engage the younger generation of a family, which can foster independence and ownership of specific initiatives.

- Time-Sensitive Events: DAFs are perfect for quick setup during time-sensitive events like selling a business or property, especially near the end of the tax year.

- Life Events: DAFs can be used during life events such as divorce, inheritance, or broader estate planning.

- Transitioning from Private Foundations: We have also seen families choose to wind down their private foundation, transferring the assets into a DAF to simplify their affairs, while preserving your family’s giving legacy.

These are just a few ways DAFs can be helpful. We encourage you to consult your Burgundy Investment Counsellor, tax advisor, or philanthropic advisor to see if a DAF might fit into your overall strategy.

This post is presented for illustrative and discussion purposes only. It is not intended to provide investment advice and does not consider unique objectives, constraints or financial needs. Under no circumstances does this post suggest that you should time the market in any way or make investment decisions based on the content. Select securities may be used as examples to illustrate Burgundy’s investment philosophy. Burgundy funds or portfolios may or may not hold such securities for the whole demonstrated period. Investors are advised that their investments are not guaranteed, their values change frequently and past performance may not be repeated. This post is not intended as an offer to invest in any investment strategy presented by Burgundy. The information contained in this post is the opinion of Burgundy Asset Management and/or its employees as of the date of the post and is subject to change without notice. Please refer to the Legal section of this website for additional information.